The goal of caretForecast is to provide tools for forecasting time series data using various machine learning algorithms.

The CRAN version with:

install.packages("caretForecast")The development version from GitHub with:

# install.packages("devtools")

devtools::install_github("Akai01/caretForecast")These are basic examples which shows you how to solve common problems with different ML models.

library(caretForecast)

#> Registered S3 method overwritten by 'quantmod':

#> method from

#> as.zoo.data.frame zoo

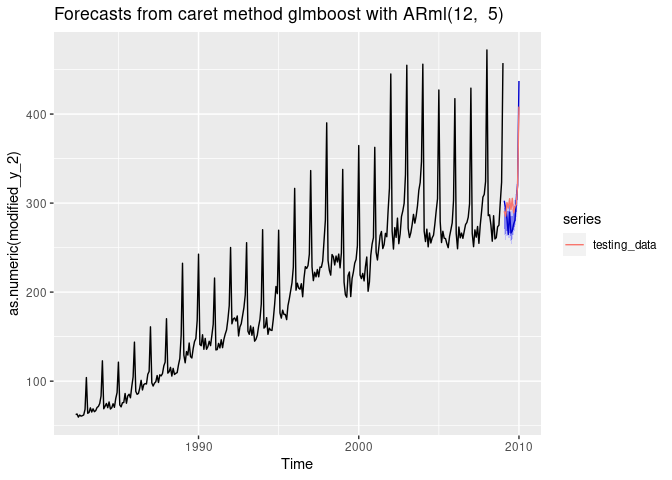

# Forecasting with glmboost

data(retail_wide, package = "caretForecast")

i <- 8

dtlist <- caretForecast::split_ts(retail_wide[,i], test_size = 12)

training_data <- dtlist$train

testing_data <- dtlist$test

fit <- ARml(training_data, max_lag = 12, caret_method = "glmboost",

verbose = FALSE)

#> Loading required package: lattice

#> Loading required package: ggplot2

forecast(fit, h = length(testing_data), level = c(80,95), PI = TRUE)-> fc

accuracy(fc, testing_data)

#> ME RMSE MAE MPE MAPE MASE

#> Training set 0.8868074 16.39661 11.65025 -0.3620986 5.702257 0.7559694

#> Test set 8.3976171 20.15546 17.20306 3.0153042 5.572722 1.1162843

#> ACF1 Theil's U

#> Training set 0.5707204 NA

#> Test set 0.3971016 0.7547318

autoplot(fc) +

autolayer(testing_data, series = "testing_data")

## NOTE : Promotions, holidays, and other external variables can be added in the model via xreg argument. Please look at the documentation of ARml.

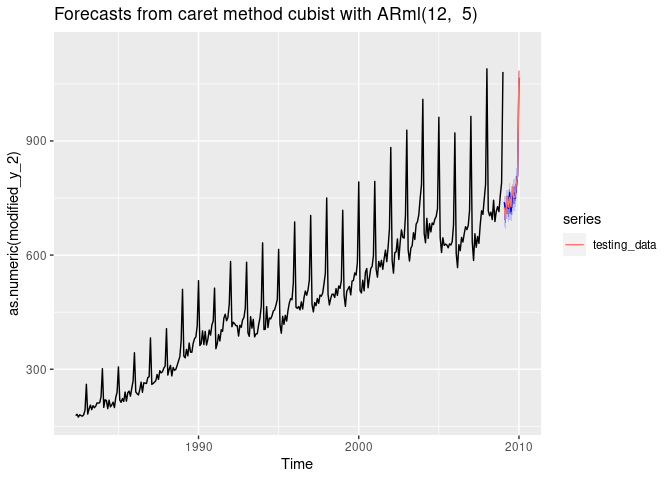

# Forecasting with cubist regression

i <- 9

data(retail_wide, package = "caretForecast")

dtlist <- caretForecast::split_ts(retail_wide[,i], test_size = 12)

training_data <- dtlist$train

testing_data <- dtlist$test

fit <- ARml(training_data, max_lag = 12, caret_method = "cubist",

verbose = FALSE)

forecast(fit, h = length(testing_data), level = c(80,95), PI = TRUE)-> fc

accuracy(fc, testing_data)

#> ME RMSE MAE MPE MAPE MASE

#> Training set 0.3452345 16.39877 12.22406 -0.08475644 2.533889 0.4073634

#> Test set 2.5562312 14.21461 12.39887 0.24907619 1.592606 0.4131888

#> ACF1 Theil's U

#> Training set 0.2309758 NA

#> Test set -0.1450719 0.1701567

autoplot(fc) +

autolayer(testing_data, series = "testing_data")

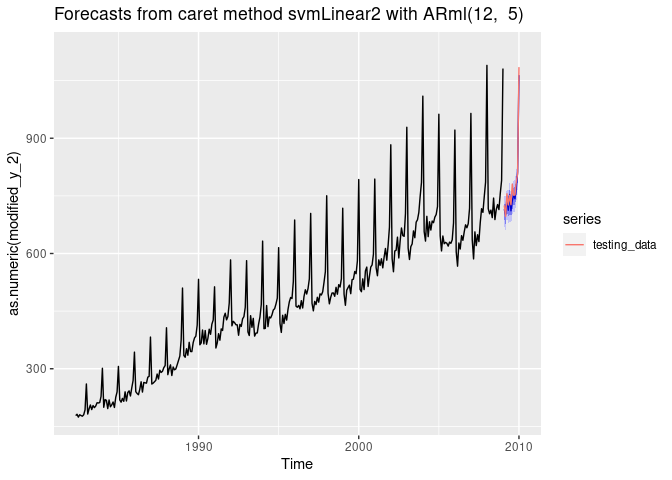

# Forecasting using Support Vector Machines with Linear Kernel

data(retail_wide, package = "caretForecast")

i <- 9

dtlist <- caretForecast::split_ts(retail_wide[,i], test_size = 12)

training_data <- dtlist$train

testing_data <- dtlist$test

fit <- ARml(training_data, max_lag = 12, caret_method = "svmLinear2",

verbose = FALSE, pre_process = c("scale", "center"))

forecast(fit, h = length(testing_data), level = c(80,95), PI = TRUE)-> fc

accuracy(fc, testing_data)

#> ME RMSE MAE MPE MAPE MASE

#> Training set 1.086666 15.67422 11.87520 0.06663619 2.497392 0.3957375

#> Test set 10.671509 16.75893 12.72986 1.33830385 1.611293 0.4242188

#> ACF1 Theil's U

#> Training set 0.09739853 NA

#> Test set -0.27328009 0.2062128

autoplot(fc) +

autolayer(testing_data, series = "testing_data")

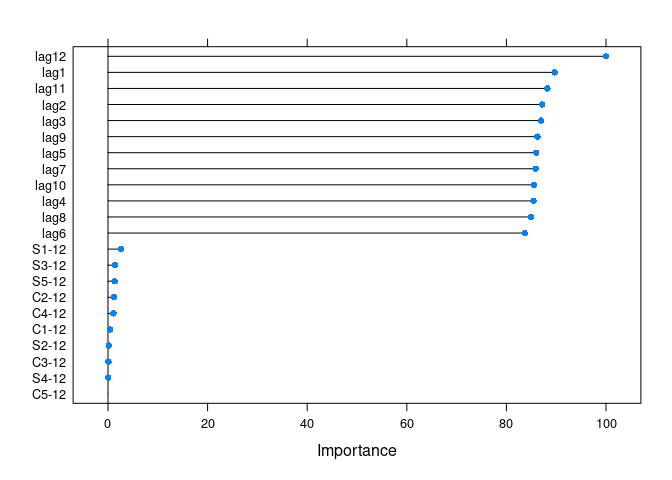

get_var_imp(fc)

get_var_imp(fc, plot = F)

#> loess r-squared variable importance

#>

#> only 20 most important variables shown (out of 22)

#>

#> Overall

#> lag12 100.00000

#> lag1 89.70809

#> lag11 88.21434

#> lag2 87.15896

#> lag3 86.95035

#> lag9 86.22539

#> lag5 85.98743

#> lag7 85.86392

#> lag10 85.56408

#> lag4 85.44561

#> lag8 84.95210

#> lag6 83.66422

#> S1-12 2.62893

#> S3-12 1.38199

#> S5-12 1.32829

#> C2-12 1.21307

#> C4-12 1.09981

#> C1-12 0.44682

#> S2-12 0.14723

#> C3-12 0.09562

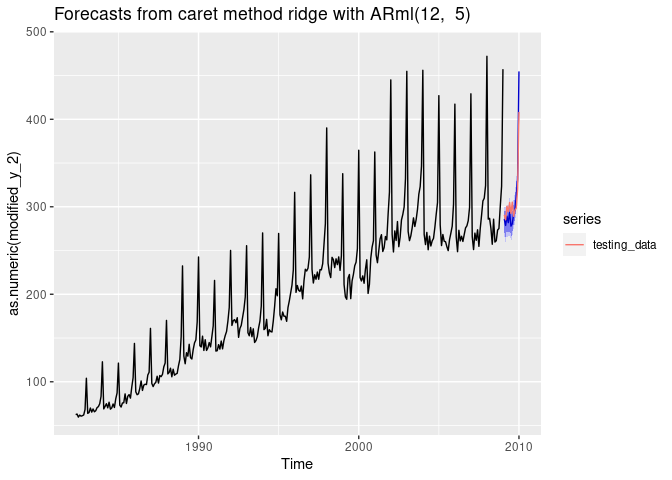

# Forecasting using Ridge Regression

data(retail_wide, package = "caretForecast")

i <- 8

dtlist <- caretForecast::split_ts(retail_wide[,i], test_size = 12)

training_data <- dtlist$train

testing_data <- dtlist$test

fit <- ARml(training_data, max_lag = 12, caret_method = "ridge",

verbose = FALSE)

forecast(fit, h = length(testing_data), level = c(80,95), PI = TRUE)-> fc

accuracy(fc, testing_data)

#> ME RMSE MAE MPE MAPE MASE

#> Training set 0.1414756 8.88367 6.44208 -0.0953757 3.126316 0.4180182

#> Test set 0.9965672 17.71459 13.30744 0.7019753 4.092068 0.8635023

#> ACF1 Theil's U

#> Training set 0.004518837 NA

#> Test set 0.389409945 0.6513039

autoplot(fc) +

autolayer(testing_data, series = "testing_data")

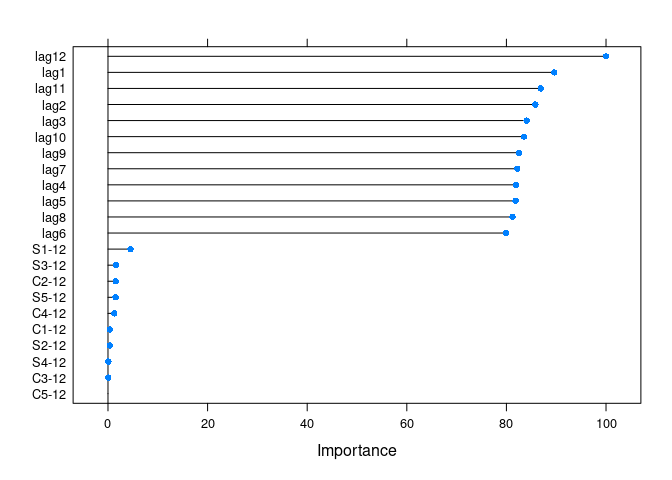

get_var_imp(fc)

get_var_imp(fc, plot = F)

#> loess r-squared variable importance

#>

#> only 20 most important variables shown (out of 22)

#>

#> Overall

#> lag12 100.00000

#> lag1 89.57697

#> lag11 86.89260

#> lag2 85.81967

#> lag3 84.07269

#> lag10 83.53358

#> lag9 82.52774

#> lag7 82.18917

#> lag4 81.93730

#> lag5 81.85290

#> lag8 81.22696

#> lag6 79.96364

#> S1-12 4.51371

#> S3-12 1.59063

#> C2-12 1.54661

#> S5-12 1.53004

#> C4-12 1.24044

#> C1-12 0.38784

#> S2-12 0.35446

#> S4-12 0.07244